Key Takeaways

- Effective date: January 1, 2026

- Tax scope: All products containing nicotine or tobacco

- Newly taxed products: Synthetic nicotine pouches, disposable e-cigarette products, nicotine-containing e-liquids

- Tax base change: From volume-based to value-based taxation

- Nicotine-containing e-cigarette products will be subject to the litter tax

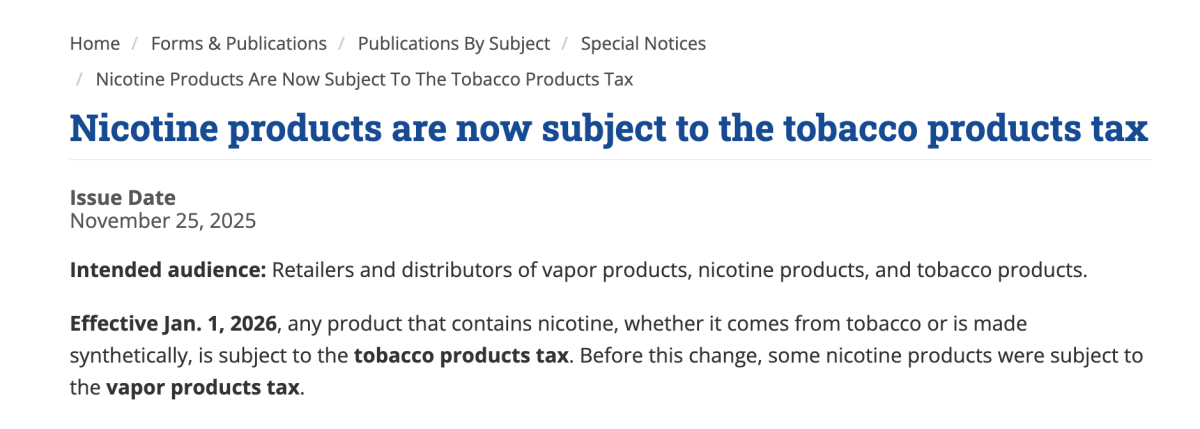

2Firsts, December 29, 2025 – According to a notice released by the Washington State Department of Revenue, effective January 1, 2026, any product containing nicotine will be subject to the Tobacco Products Tax, regardless of whether the nicotine is derived from tobacco or synthetically produced. Previously, some nicotine products were subject to the vapor products tax.

The Tobacco Products Tax applies to all products containing tobacco or nicotine, including cigars, pipe tobacco, chewing tobacco, e-cigarettes, synthetic nicotine pouches, nicotine e-cigarette products, and any other products containing tobacco or nicotine in any form. Newly taxed products include synthetic nicotine pouches that were previously untaxed, disposable e-cigarette products, and nicotine-containing e-liquids.

The regulations also clarify that “tobacco products” do not include cigarettes, nor do they include any drug, device, or combination product approved for sale by the U.S. Food and Drug Administration as of December 31, 2024.

The Tobacco Products Tax is calculated based on the taxable selling price of nicotine products. According to reports by NBC Right Now and KOMO News, the tax rate for all nicotine and tobacco products is 95% of the selling price.

Retailers and distributors must report the value of their existing inventory of nicotine products on the first return filed after January 1, 2026. A one-time line item will be added to the return: “Pre-existing inventories of nicotine products as of January 1, 2026.”

If a product is purchased from a non-affiliated seller, the purchase price should be used as the selling price. If the retailer or distributor is affiliated with the manufacturer or distributor, the actual selling price must be used.

The vapor products tax is calculated based on e-liquid volume and container type, while the Tobacco Products Tax is based on the value of the product in its original package or container. When calculating the Tobacco Products Tax on nicotine-containing e-cigarette products, the selling price must be used rather than volume.

In addition, the litter tax applies to all tobacco products. Previously, e-cigarette products were not subject to the litter tax; however, following the implementation of the new rules, nicotine-containing e-cigarette products will be included. No credit will be provided for vapor products tax previously paid.

Businesses that sell tobacco products are required to obtain a tobacco retail endorsement for each sales location, which can be added to their business license through a MyDOR account.

Cover image source: the Washington State Department of Revenue

We welcome news tips, article submissions, interview requests, or comments on this piece.

Please contact us at info@2firsts.com, or reach out to Alan Zhao, CEO of 2Firsts, on LinkedIn

Notice

1. This article is intended solely for professional research purposes related to industry, technology, and policy. Any references to brands or products are made purely for objective description and do not constitute any form of endorsement, recommendation, or promotion by 2Firsts.

2. The use of nicotine-containing products — including, but not limited to, cigarettes, e-cigarettes, nicotine pouchand heated tobacco products — carries significant health risks. Users are responsible for complying with all applicable laws and regulations in their respective jurisdictions.

3. This article is not intended to serve as the basis for any investment decisions or financial advice. 2Firsts assumes no direct or indirect liability for any inaccuracies or errors in the content.

4. Access to this article is strictly prohibited for individuals below the legal age in their jurisdiction.

Copyright

This article is either an original work created by 2Firsts or a reproduction from third-party sources with proper attribution. All copyrights and usage rights belong to 2Firsts or the original content provider. Unauthorized reproduction, distribution, or any other form of unauthorized use by any individual or organization is strictly prohibited. Violators will be held legally accountable.

For copyright-related inquiries, please contact: info@2firsts.com

AI Assistance Disclaimer

This article may have been enhanced using AI tools to improve translation and editorial efficiency. However, due to technical limitations, inaccuracies may occur. Readers are encouraged to refer to the cited sources for the most accurate information.

We welcome any corrections or feedback. Please contact us at: info@2firsts.com